We (Argo SE) have been helping to design and build the software systems for regulated equity, commodity and derivatives exchanges, crypto, FX and energy market operators, ATSes, dark pools, brokers, hedge funds and HFT shops in US and overseas. We employ the brightest software engineers. We are experts in all aspects of financial technology, trading and exchange technology workflows: order management and routing, trade execution, matching algorithms, exchange connectivity, market data distribution and handling, risk management and control, account and portfolio management, automatic trading and market making.

We code in C++, C#, JavaScript, use high-performance code optimization techniques, multithreading on Windows and Linux platforms, advanced TCP, UDP and reliable multicast networking. We are experts in FIX, FIX/FAST, MDP 3, proprietary order management, market data protocols. We with all major RDBMSes and many popular C++ and C# frameworks including Boost, QT, ACE, DevExpress.

There is no project too small or too big for Argo! Our development fees are very competitive!

Please contact us via info@argocons.com for more information or inquire about our free design session.

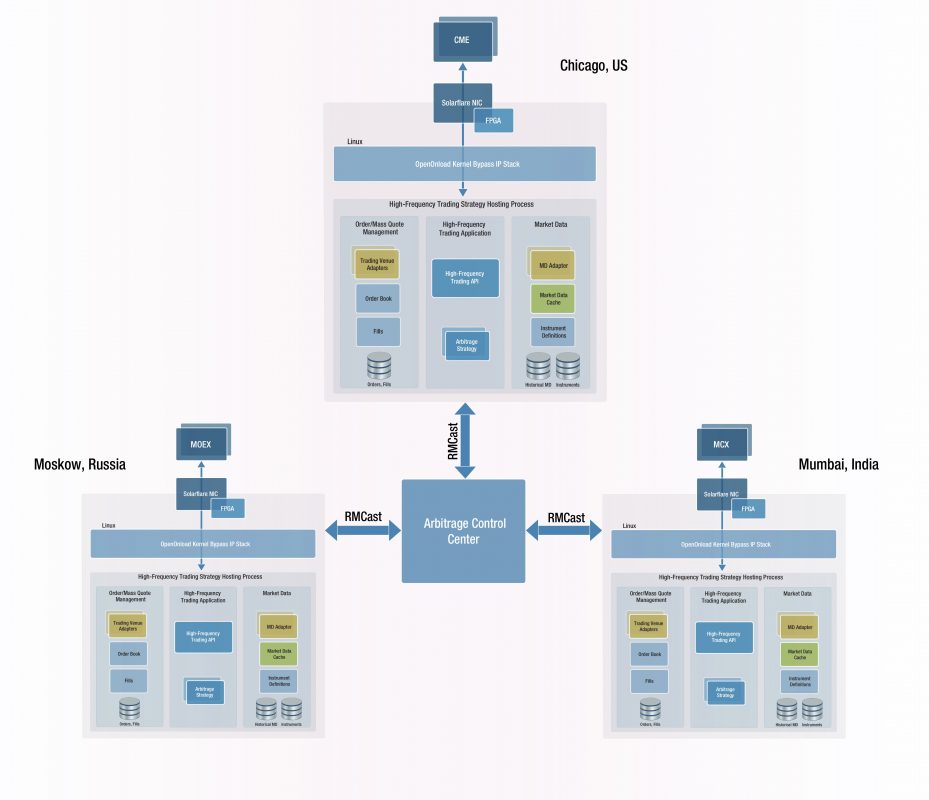

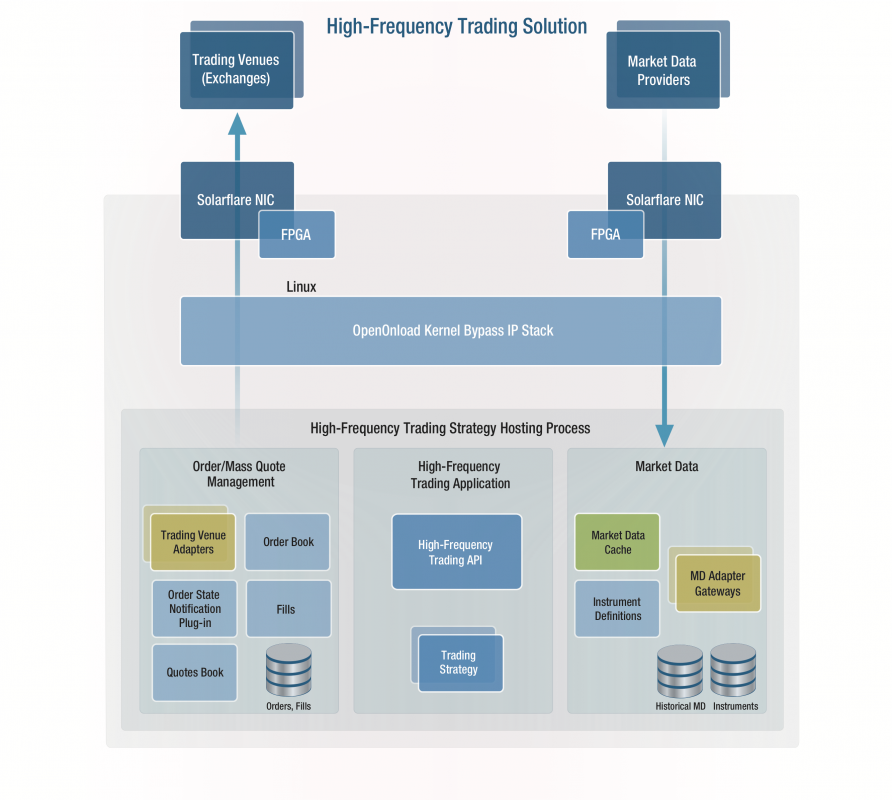

We also sell well designed and tested electronic trading components. Our flagship product Argo Trading Platform (ATP) is a generic multi-asset electronic trading solution that serves as a solid technological base for various types of businesses – from regulated equity and commodity exchanges, crypto exchanges, market makers to brokers, hedge funds and high-frequency traders. We have certified and integrated ATP with major trading venues and market data providers, including: CME, ICE, CBOT, NSE, MCX, MCX-SX, MOEX, Liffe, EUREX, Arca, Bats, many US dark pools and ATSes, BitMEX, HotSpot, Currenex, EBS, IKON, SIAC/Opra, TenFore, OpenTick, CQG.

ATP comes with ultra-fast order management system (OMS), user friendly desktop and web-based trading screens, charting and technical analysis, algorithmic trading servers, market data distribution and historical market data facility, risk management system, high capacity/low latency matching engine, Trading APIs, High Frequency Trading (HFT) framework, reliable multicast and TCP based messaging system RMCast.

ATP integration team offers assistance in connecting to electronic systems of market participants and regulators for pre-trade risk check, trade confirmation, allocations, regulatory reporting and clearing via MQ, FIX, FpML, and proprietary protocols and APIs.

ATP was successfully used in implementation equity, fixed income and commodity exchanges, OTC, FOREX, cryptocurrency, commodity (spot and futures), energy markets, ATSes, brokerage and prop trading systems.

Source code and binary licenses, SaaS and hosting arrangements are available.