High-Frequency Trading (HFT) Framework

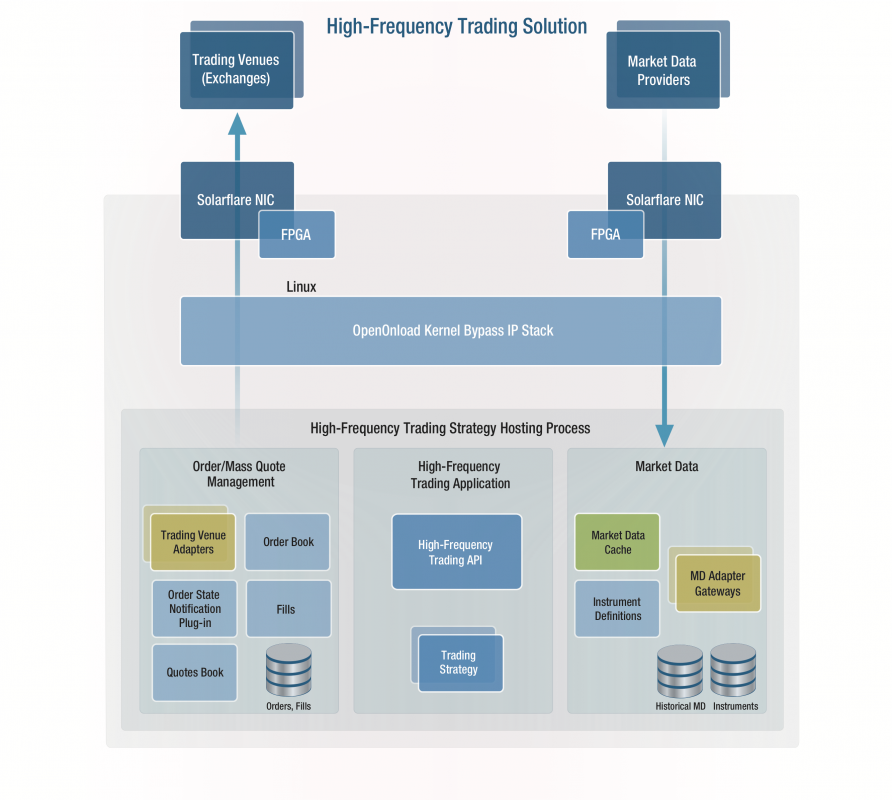

Argo SE announces availability of High-Frequency Trading (HFT) solution. Argo HFT integrates Argo Trading API, ultra-fast Order Management System and Market Data Distribution with trading venue (CME iLink, MOEX FIX, NCX/MCX FIX and others) and market data (CME MDP 3, MOEX FIX/FAST, NCX/MCX, ICE) adapters. The solution comes in one lightweight Linux package The solution comes in one lightweight Linux package with network interface cards by Solarflare and OpenOnload kernel-bypass IP stack. Argo HFT provides seamless integration with other components of Argo Trading Platform including Argo Trader (trading front-end) and Risk Management Facility

Achieving a sub-microsecond latency may be difficult in conventional trading applications. We have “collocated” trading API, order management and market data modules in one process, eliminated IOC-related latencies, applied a number of performance optimization techniques:

- build on Linux, taking advantages of myriads OS-specific optimization tricks

- use the best of the breed network technology and kernel bypass IP stack from Solarflare

- eliminate data copying – whenever possible

- pre-serialize FIX messages directed to trading venue

- refactor data structures to facilitate optimal use of processor cache

- apply lock-less and block-less design patterns, eliminating OS signaling latency whenever it’s possible

- utilized OS scheduler interfaces to complete minimize non-deterministic behavior of standard thread scheduling algorithms

Our tick-2-order latency satisfies the needs of the most demanding HFT and Market Making applications. Argo HFT is written on C++ and can be used with various FPGA solutions. Source Code and binary licenses are available. Support and consulting services are available. Please contact us for more information.