Algorithmic Trading

Argo Algorithmic Trading offerings include Argo Robots – server-based automatic trading strategy hosting system and High Frequency Trading (HFT) framework. Both solutions are seamlessly integrated with Argo Trading Platform components – Argo Trader, Order Router, MD Feeder and Risk Manager Server. Designer of automatic strategy (for HFT or MFT) writes his code using our powerful ATP Trading API. API includes a complete set of order management, market data interfaces as well as a number of mathematical and statistical functions that are necessary for technical analysis based algorithms. The strategy is built into a dynamic link library (we provide examples) and injected into the Argo Robot Server. Here is Argo Robot Developer’s Guide.

Argo Algorithmic Trading framework is written on C++ for optimal performance and portability. Source code licenses are available.

For web-based front-end developers, we provide RESTful Trading API.

Please contact us for information regarding new ATP trading strategy backtesting facilities.

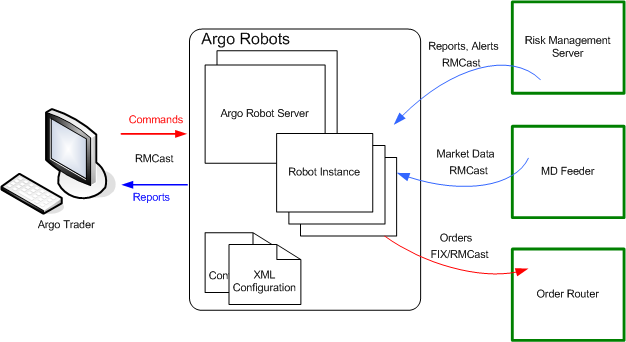

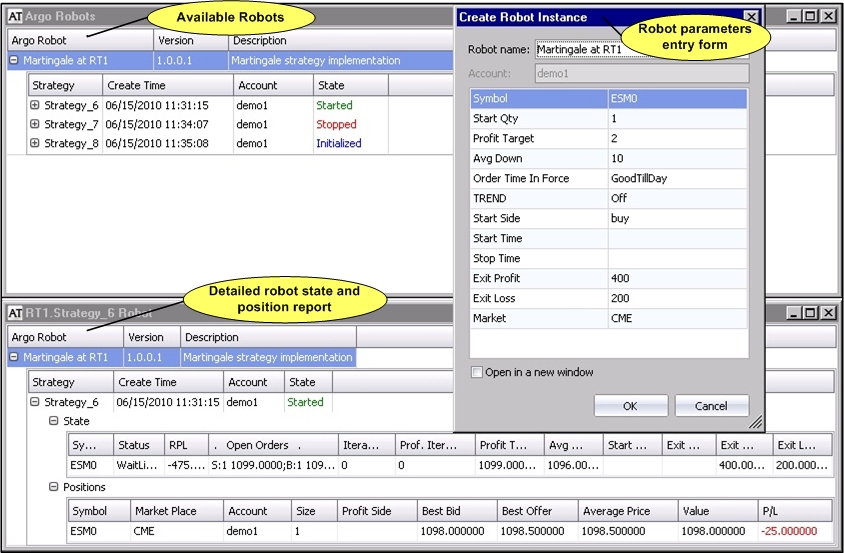

Argo Robot Control Facilities

In Argo Robots environment a trader starts a new trading strategy instance using Argo Trader robot control panel. Robot’s start-up parameters are submitted to Argo Robots hosting server. The hosting server starts the strategy process (a robot). Robot receives market data, risk control messages and sends orders to the markets. It reports its status back to Argo Trader. For each running robot Argo Trader displays positions, P&L and, also, robot-specific information. Trader can control robot execution, stop and restart robot by sending commands and modifying robot parameters — on the fly!

Robot control facilities can also be integrated into your own application using our Argo Robot Control API.

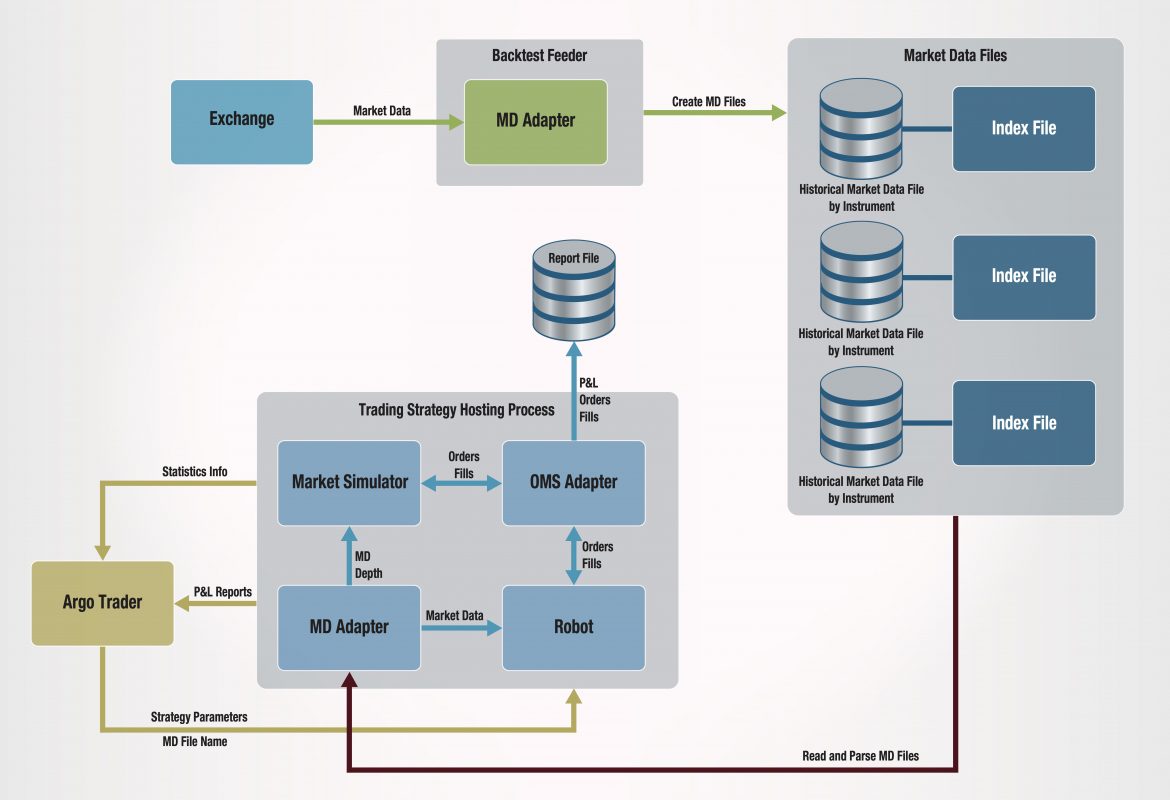

Backtesting and Forward Testing

Argo offers a robust and functionally rich backtesting and forward testing facilities.

Our forward testing facility is based on market simulation module of the Argo Matching Engine. This infrastructure, which includes both backtesting and forward testing components, enables traders to rigorously test and refine their algorithms under realistic market conditions, ensuring optimal performance and reliability.

Custom Automatic Trading Development

We have accumulated a wealth of experience building automatic trading and market making strategies using our powerful Trading API and HFT framework. Please send us a message to inquire about our custom development services and provide contact information. We will get back to you promptly.

AI-driven Trading

We are also working on an AI-driven trading framework that applies supervised learning for market regime classification, ranks strategy candidates based on historical performance metrics, and uses Retrieval-Augmented Generation (RAG) with a fine-tuned Code LLaMA model to auto-generate ATP-compatible C++ strategy code. We plan to release the first version by the third quarter of 2025.