Argo Trader

Argo Trader was designed to provide ultimate speed of trading operations and technical analysis. Argo Trader is seamlessly integrated with the Platform server components MD Feeder, OMS/Order Router, Risk Manager Server and Argo Robots Algorithmic Server. Traders monitor market data and positions, control their orders and automatic trading strategies in real-time.

Argo Trader is written on C#. Source code licenses are available.

Argo Trader Features

- real-time and historical market data charts supporting number of technical indicators and studies;

- inside market, market statistics, aggregated market depth, and Level 2 views;

- accounts and positions monitoring;

- order entry form supporting Market, Limit, Stop-Loss, Stop-Limit, Iceberg, Stop-Loss-Take-Profit, and Market-If-Touched orders, as well as “one cancel the other” and “if-done” combinations;

- Day, GTC, GTD, GFS, IOC, FOK, AON and other time-in-force options;

- pre-trade risk control;

- order and order history details views;

- trading on behalf of multiple accounts;

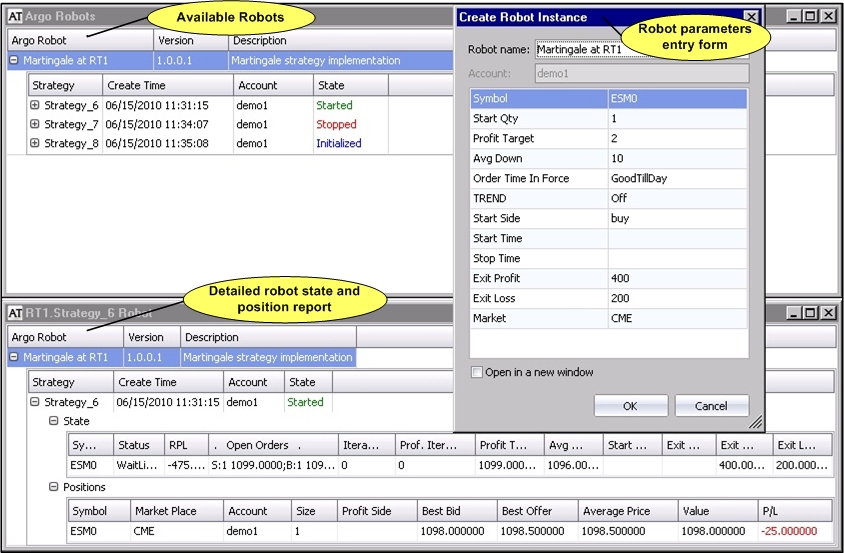

- algorithmic trading panel allows real-time control of automatic strategies (Argo Robots) executions;

- configurable alerts

- configurable news view;

- integrated transactions and positions reports;

- chat with administrator facility;

- secure communication over public networks;

- embedded connection QOS monitoring facility.

Argo Trader is user-friendly and fully customizable application. Traders arrange market data, order history, positions, charts, news, all data items and color schema in any way they like.

We provide white labeling for free. You can also purchase Argo Trader source code by paying a one-time license fee and then distribute the application to your clients without paying additional fees.

To evaluate our Trading Platform please send us a request and provide contact information. We will get back to you shortly.